Beginner’s Guide to Mortgage

Written: Editor | April 4, 2023

Finding the Right Mortgage

Finding the right mortgage can seem like a daunting task, especially for first-time homebuyers. However, with the right knowledge and guidance, you can navigate the mortgage market and make an informed decision. Here is a beginner's guide to help you get started.

Factors to consider when choosing a mortgage

When choosing a mortgage, there are several key factors to consider:

-

Interest rates: The interest rate will determine the cost of borrowing and affect your monthly mortgage payments. It's important to compare rates from different lenders to ensure you secure the best possible deal.

-

Loan term: The loan term refers to the length of time you'll have to repay the mortgage. Shorter terms typically come with higher monthly payments but result in lower overall interest costs.

-

Down payment: The size of your down payment will impact the amount you need to borrow and can affect the interest rate and mortgage insurance requirements. Generally, a larger down payment will result in a lower monthly payment and better loan terms.

Comparison of fixed-rate and adjustable-rate mortgages

There are two main types of mortgages: fixed-rate and adjustable-rate mortgages (ARMs).

-

Fixed-rate mortgages: With a fixed-rate mortgage, the interest rate remains constant throughout the loan term. This provides stability and predictability, making it easier to budget for your monthly payments.

-

Adjustable-rate mortgages: ARMs have an initial fixed-rate period, after which the interest rate may fluctuate periodically. These mortgages often have lower initial rates, but they can increase over time, which can be a risk if rates rise significantly.

Understanding mortgage terms and conditions

Before signing any mortgage agreement, it's crucial to understand the terms and conditions. Consider the following:

-

Prepayment penalties: Some mortgages may impose penalties if you pay off the loan early. Be sure to read the fine print and understand any potential penalties.

-

Loan origination fees: These are fees charged by the lender for processing the loan. It's essential to understand the costs associated with obtaining the mortgage.

-

Mortgage insurance: Depending on your down payment amount, you may be required to pay for mortgage insurance. This protects the lender in case the borrower defaults on the loan.

Taking the time to understand these factors and terms will empower you to make an informed decision when choosing a mortgage that aligns with your financial goals and needs.

Applying for a Mortgage

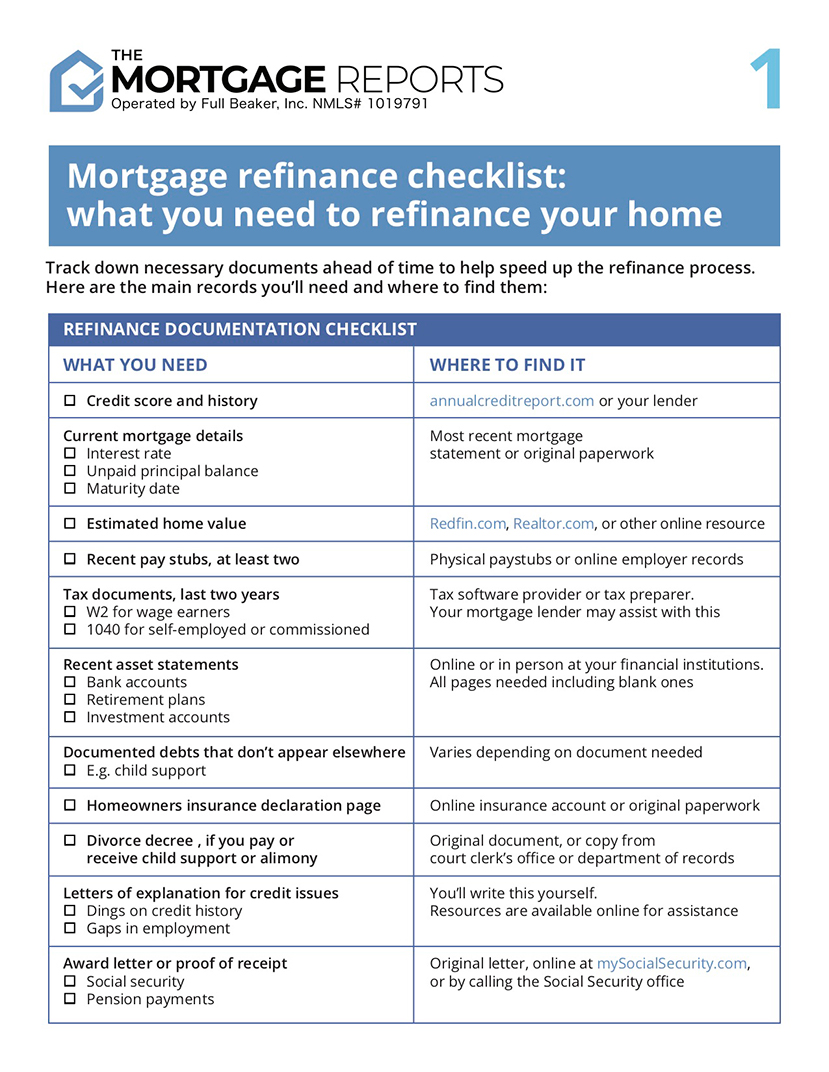

Essential documents for mortgage application

When applying for a mortgage, there are several key documents that lenders typically require. These documents help the lender assess your financial situation and determine your eligibility for a mortgage. Here are some important documents to prepare:

-

Proof of income: This includes recent pay stubs, W-2 forms, and tax returns. Lenders want to see a stable income to ensure that you can afford the mortgage payments.

-

Proof of assets: Provide bank statements, investment account statements, and any other documentation that shows your savings and assets. Lenders want to see that you have enough funds for the down payment and closing costs.

-

Employment verification: You may need to provide employment verification letters or contact information for your employer. Lenders want to verify that you have a stable job and income.

-

Credit history: Lenders will review your credit history and may request your credit reports from the major credit bureaus. It's important to have a good credit score to qualify for favorable mortgage rates.

The mortgage pre-approval process

Before house hunting, it's a good idea to get pre-approved for a mortgage. Getting pre-approved gives you an idea of how much you can afford and makes you a more attractive buyer. Here's what the pre-approval process typically involves:

-

Submit an application: You'll need to complete a mortgage application and provide the necessary documents (as mentioned above).

-

Credit check: The lender will review your credit history and assess your creditworthiness.

-

Income and asset verification: The lender will verify your income, employment, and assets to ensure you meet their requirements.

-

Pre-approval letter: If you meet the lender's criteria, you'll receive a pre-approval letter stating the maximum loan amount you qualify for.

Understanding the mortgage application fees

When applying for a mortgage, it's important to understand the various fees involved. Here are some common fees you may encounter:

-

Application fee: This fee covers the cost of processing your mortgage application. It can range from $100 to $500 or more, depending on the lender.

-

Appraisal fee: Lenders typically require an appraisal to determine the value of the property. The appraisal fee can vary but is usually around $300 to $500.

-

Origination fee: This fee is charged by the lender for processing the loan. It's typically a percentage of the loan amount, ranging from 0.5% to 1% or more.

-

Closing costs: These are fees associated with the closing of the loan, including title insurance, attorney fees, and prepaid interest. Closing costs can vary but are typically around 2% to 5% of the loan amount.

It's important to review the fees and costs associated with your mortgage application and compare them across different lenders to ensure you're getting the best deal.

:max\_bytes(150000):strip\_icc()/mortgage-process-explained-5213694\_final-a7545c4d1aaf4d9bb09c48611b16e9c3.jpg)

Navigating the Mortgage Process

When it comes to buying a home, obtaining a mortgage can seem like a daunting task, especially for beginners. However, understanding the mortgage process is crucial for making informed decisions and securing the best deal.

Mortgage underwriting process

Before a lender approves your mortgage application, it goes through the underwriting process. During underwriting, the lender evaluates your financial situation, credit history, employment and income stability, and the property's value. They use this information to determine your eligibility for a mortgage and the terms of the loan. Be prepared to provide documentation such as tax returns, pay stubs, bank statements, and proof of assets.

Mortgage closing process and associated costs

The mortgage closing process is the final step before you officially become a homeowner. It involves signing the mortgage agreement, completing paperwork, and paying closing costs, which include appraisal fees, attorney fees, title insurance, and loan origination fees. It's important to carefully review and understand the terms and conditions outlined in the mortgage agreement before signing.

Important considerations before signing the mortgage agreement

Before committing to a mortgage, there are several key considerations to keep in mind. Firstly, determine the type of mortgage that suits your needs – fixed-rate or adjustable-rate. Consider your financial goals, budget, and risk tolerance. Additionally, evaluate your ability to make a down payment and factor in the ongoing costs such as property taxes, insurance, and maintenance.

It is also advisable to compare mortgage offers from different lenders to ensure you are getting the best interest rates and terms. Consult with a reputable mortgage broker or financial advisor who can guide you through the process and help you make an informed decision.

By familiarizing yourself with the mortgage process, you can navigate through it more confidently. Remember, buying a home is a significant financial commitment, and taking the time to educate yourself about mortgages will ultimately result in a better home-buying experience.

:max\_bytes(150000):strip\_icc()/dotdash-TheBalance-calculate-mortgage-315668-final-fd8c0ed392cd40118439cd1c23317e99.jpg)

Managing Your Mortgage

Making regular mortgage payments

When it comes to managing your mortgage, consistently making regular payments is crucial. Your mortgage payment is typically due monthly and includes the principal and interest. It's important to set a budget and prioritize your mortgage payment to avoid any late payments or penalties. Many homeowners find it helpful to set up automatic payments to ensure they never miss a due date.

Understanding the role of escrow accounts

An escrow account is a separate account that holds funds to pay for ongoing property expenses, such as property taxes and insurance. When you make your monthly mortgage payments, a portion of the funds goes into your escrow account. The lender then uses these funds to pay your property taxes and insurance premiums on your behalf. It's important to understand how your escrow account works and regularly review your statements to ensure the correct amount is being collected and paid.

Options for refinancing your mortgage

Refinancing your mortgage can be a beneficial option for homeowners who want to take advantage of lower interest rates or improve their financial situation. When you refinance your mortgage, you essentially replace your existing loan with a new one. This can help you secure a lower interest rate, reduce your monthly payment, or change the terms of your loan. However, refinancing does come with certain costs, such as closing fees and prepayment penalties. It's important to carefully consider these factors and weigh the potential benefits before deciding to refinance.

Overall, managing your mortgage requires responsible payment habits, understanding escrow accounts, and considering the option of refinancing when appropriate. By staying informed and making informed decisions, you can effectively manage and navigate the world of mortgages.

Mortgage Tips and Pitfalls to Avoid

Common mistakes to avoid when getting a mortgage

When it comes to obtaining a mortgage, making mistakes can have serious consequences. Here are some common pitfalls to avoid:

-

Not shopping around: Many first-time buyers make the mistake of not exploring multiple lenders and mortgage options. By doing thorough research, you can find the best interest rates and terms that suit your financial situation.

-

Overextending your finances: Be realistic about your budget and avoid taking on more debt than you can comfortably handle. Remember, owning a home involves other expenses like property taxes, insurance, and maintenance costs.

-

Not checking your credit score: Your credit score plays a crucial role in determining your eligibility for a mortgage. Before applying, check your credit report for any errors or negative items that need to be addressed.

Tips for improving your chances of getting approved

To increase your chances of getting approved for a mortgage, follow these tips:

-

Save for a down payment: Most lenders require a down payment. Start saving early to ensure you have enough funds for a substantial down payment, which can help lower your interest rate.

-

Improve your credit score: Pay your bills on time, reduce your debt-to-income ratio, and avoid applying for new credit cards or loans in the months leading up to your mortgage application.

-

Get pre-approved: Getting pre-approved for a mortgage can give you a competitive advantage when shopping for a home. It shows sellers that you are serious about buying and have the financial means to do so.

Mortgage-related scams and how to protect yourself

Unfortunately, mortgage-related scams are common. Here are some ways to protect yourself:

-

Be cautious of unsolicited offers: Be wary of unsolicited calls, emails, or letters offering mortgage assistance or promising lower interest rates. Legitimate lenders do not typically contact you out of the blue.

-

Research mortgage companies: Before working with a lender, research their reputation, read reviews, and check if they are registered with your local regulatory agency.

-

Get everything in writing: Always get the terms of your mortgage agreement in writing and read the fine print carefully. If something seems too good to be true, it probably is.

By avoiding common mistakes, following helpful tips, and being vigilant against scams, you can navigate the mortgage process with confidence.

Conclusion

In conclusion, understanding the basics of mortgages is essential for first-time homebuyers. By familiarizing yourself with the key concepts discussed in this guide, you'll be better equipped to navigate the mortgage process and make informed decisions. Remember to consider your financial situation, creditworthiness, and long-term goals when choosing a mortgage option.

Summary of key points discussed

- Importance of creditworthiness: Lenders assess your credit score and financial history to determine your eligibility for a mortgage and the interest rate you'll qualify for.

- Types of mortgages: Common mortgage options include fixed-rate mortgages, adjustable-rate mortgages, and government-backed mortgages like FHA and VA loans.

- Loan-to-value ratio: This ratio represents the amount of the loan compared to the appraised value of the property.

- Down payment: The initial upfront payment made towards the purchase of a home, typically ranging from 3% to 20% of the purchase price.

- Mortgage pre-approval: Getting pre-approved for a mortgage can give you an advantage in the homebuying process by demonstrating your financial readiness to sellers.

Next steps in your mortgage journey

If you're ready to take the next steps in your mortgage journey, consider the following:

- Research: Continue researching mortgage options, interest rates, and lenders to find the best fit for your needs.

- Get pre-approved: Contact lenders for pre-approval to determine your budget and enhance your position as a serious buyer.

- Find a real estate agent: Engage the expertise of a real estate agent to guide you through the home search and purchase process.

- Complete the mortgage application: Gather the necessary documents and submit a mortgage application to your chosen lender.

Frequently Asked Questions about mortgages

- What credit score is needed to qualify for a mortgage? Most lenders require a credit score of at least 620, but scores above 700 generally qualify for better interest rates.

- How much should I save for a down payment? Saving 20% of the home's purchase price can help you avoid private mortgage insurance (PMI), but there are loan options available with lower down payment requirements.

- What documents are needed for a mortgage application? Generally, you'll need proof of income, bank statements, tax returns, and identification documents.

- How long does the mortgage process take? The mortgage process typically takes 30 to 45 days from application to closing, but it can vary based on the lender and complexity of the transaction.

Remember to consult with a mortgage professional for personalized advice based on your specific situation.